Just as the energy industry is rapidly changing, so are the methods for acquiring low-cost funding. Utilities can leverage the unique capabilities of green bonds as an economic and transparent accelerant for carbon reduction.

Green bonds are a debt instrument where organizations specifically earmark capital for the deployment of sustainable projects. These bonds share a similar structure with traditional bonds, but uniquely require impact reporting, detailing of capital allocation, and other certifications that create a new asset class. Those green projects that meet the Green Bond Principles set forth by the International Capital Markets Association are highly sought after by investors around the world.

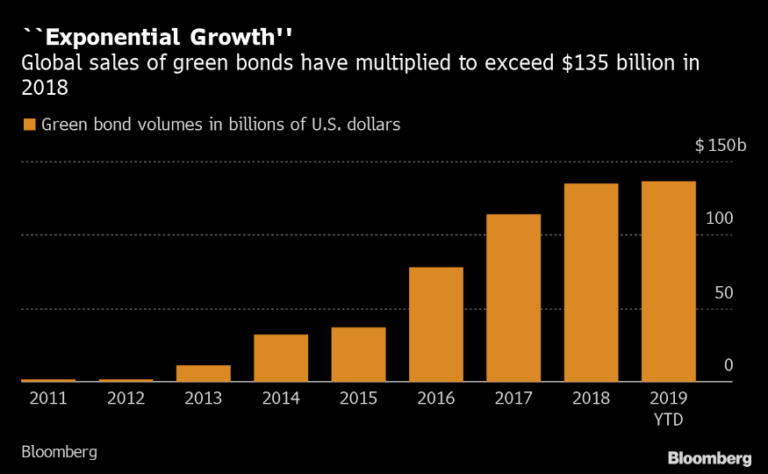

Through green bonds, issuers gain immediate access to a capital market with low rates, and investors can effectively and securely increase the amount of funds directed to sustainability – helping both to meet their own Environmental, Social, and Governance (ESG) criteria and goals. Since the first green bond issuance in 2008, the market has substantially developed, and the demand for green bonds has increased exponentially — surpassing $1 trillion in cumulative issuance in 2020.

Why green bonds?

Recent evidence shows that green bonds are developing a pricing advantage, called a “greenium” against comparable conventional bonds. While the two types of bonds are normally similarly priced, green bonds have higher margins of oversubscription, indicating substantial investor interest. For the issuer, higher demand for a project means lower borrowing costs, and lower borrowing costs equates to reduced expenditures for the development. In other words, green bonds receive lower interest rates on financing than an equivalent standard project.

The results speak for themselves. Market reports in the second half of 2020 from the Climate Bonds Initiative indicate green bonds issued in Europe and the U.S. achieved higher book cover and spread compression than vanilla equivalents, on average. They report that 70% of European green bonds issued during this period showed a greenium. Furthermore, UBS analysts expect green bonds to show “lower volatility and smaller drawdowns” during stressful market periods.

Utilities, corporations, and green bonds

The expected continued growth in the green bond market presents an opportunity for all players in the energy industry. For example, in August 2020, Tucson Electric Power successfully issued a green bond worth $300 million to finance the cost of the 250 MW capacity Oso Grande wind farm in southeast New Mexico. They earned an A- credit rating and achieved an impressive coupon rate of 1.5%.

Conventional renewable energy solutions are only the beginning. Geysers Power Company issued a $900 million green bond in June 2020 to finance investments into geothermal plants. They secured capital at London Inter-bank Offered Rate (LIBOR) +2.0% per annum. Tohoku Electric Power Company, located in Japan, issued a $45.4 million green bond to finance geothermal and wind plants in their operating region and secured a 0.31% coupon rate.

Green bonds are not isolated to projects at their onset. Companies can leverage green bonds to improve their financial situation for assets acquired previously. One example of a corporation dynamically implementing a green bond is Goldman Sachs. In October of 2020, they issued a $500 million green bond at a 3.7% coupon rate to refinance their acquisition of over 1 MW capacity of solar assets across the U.S.

Beyond clean electric power, green bonds are suitable for initiatives spanning from waste management to energy efficiency, alternative renewable energies, clean transportation, water and resource management, and more. Green bonds can help bridge the gap between finance and ESG solutions. Overall, only 56% of green bonds in 2020 were allocated to investors describing themselves as having green or ESG mandates. Although green bonds originated as a financial instrument to meet the demands of ESG investors, they are now equally sought after by those without any mandate or criteria for their high performance and security. The message that investors are sending is clear: for utility companies and other leaders in the clean energy industry, now is the time to investigate green bonds. Welcome to the future of project funding.

About the Authors

The Green Bank of Colorado (GBC) is a Public Benefit Corporation built to drive green bond success. With increased demand from investors, access to capital at low rates and long terms, the ability to tangibly demonstrate ESG commitment, and the potential for pricing advantages, GBC believes that green bonds will become central to institutions of tomorrow.

As firms look for more opportunities to direct their capital towards secure and profitable investments that fit criteria for ESG advancement, it is our duty to inform individuals, companies, utilities, and municipalities about green bonds. We can help at the project or institutional level, serving as a free resource to adapt green bond frameworks to your unique needs. To connect or to find more information, please visit www.greenbankofco.com